Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Both equities and bonds posted one of their best summers in recent history

- As tariff pressures intensify, selectivity among sectors becomes more important

- As the Fed navigates labor weakness and inflation, we expect two cuts by YE25

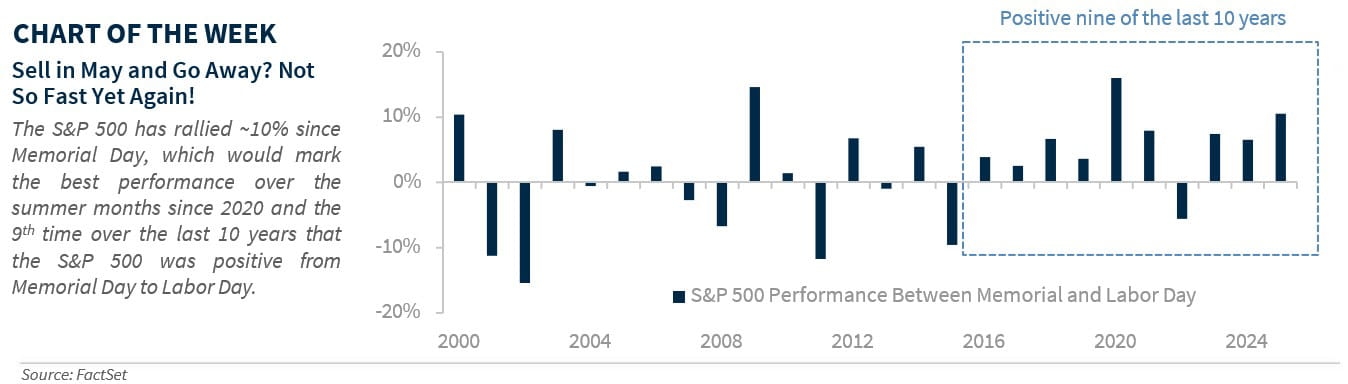

Don’t Worry, Be Happy! Heading into summer, markets faced a wave of uncertainty—from shifting tariffs and debt ceiling debates to questions around the fate of the ‘Big, Beautiful Bill.’ The challenges were hard to miss as the ‘wall of worry’ intensified. Yet, despite these headwinds, financial markets pushed through and even outperformed our expectations: the S&P 500 climbed 10.1%, while the Bloomberg Aggregate US Bond Index has added 2.7% since Memorial Day. Once again, this shows that the old adage, “Sell in May and go away,” hasn’t proven to be very accurate. But as we have noted in the past, staying invested—rather than timing the market based on seasonal trends—has historically led to stronger long-term results. Below, we break down this summer’s impressive gains and share our perspective on what we believe lies ahead for the broader equity market, sectors, and bonds.

- Equity Returns ‘Delight’ Investors This Summer | Once again, the “Sell in May and go away” strategy missed the mark. From a return perspective, this summer (e.g., the period between Memorial Day and Labor Day) was a summer to remember for equity investors. If the S&P 500 holds its 10.1% gain since Memorial Day, it would be the best summer since 2020—and the second-best since 2009. Impressively, this marks the ninth time in the past ten years that the index has posted summer gains. Volatility was also surprisingly mild: despite some recent shifts as investors have rotated out of Tech, the S&P 500’s largest pullback, thus far, has been just 2.4%—the smallest since 2017 and well below the historical average of ~7%. Gains were widespread. Small-cap stocks (Russell 2000) jumped ~12%, their best summer since 2020. International markets also shined, with developed (MSCI EAFE) and emerging (MSCI EM) markets up ~6% and ~9%, respectively, in USD terms. These gains were fueled by encouraging trade developments, the passage of the ‘Big, Beautiful Bill’, lower than feared tariffs, and resilient corporate fundamentals highlighted throughout the 2Q25 earnings season.

Looking ahead: As pre-tariff inventories wind down, and the August 7 tariffs feed through supply chains, the full impact on the economy and earnings has yet to unfold. With valuations stretched, technical indicators (e.g., RSI, put/call ratios) elevated, and sentiment measures (e.g., % of investors who expect a rise in stock prices) running high, slowing growth and earnings headwinds could lead to higher volatility in the months ahead—especially after the S&P 500’s nearly 30% rally from April lows. That’s why we remain cautious in the near term.

- ‘Positive’ Returns And Muted Dispersion Among Sectors | Despite the sharp moves in the S&P 500 this year, differences in performance across sectors have been surprisingly mild. For instance, the top-performing sector YTD—Industrials, up 15%, is only ~15% ahead of the weakest, Consumer Discretionary, which is slightly negative at -0.6%. If this trend holds, it will mark the narrowest gap between sector returns in any year since at least 1995. This low dispersion continued through the summer, with all 11 S&P 500 sectors posting gains—the first time that’s happened since 2016. Tech led the way, up 17%, while Consumer Staples trailed with a 1% increase.

Looking ahead: As the effects of tariffs continue to work their way through the economy and corporate earnings, we expect greater divergence across sectors—separating future winners from laggards. For example, as growth cools, sectors with long-term secular tailwinds—like Tech, Industrials, and Health Care—should prove more resilient than those tied to a weakening consumer. Sectors in the ‘goods’ portion of the economy (e.g., Consumer Staples and Consumer Discretionary) will also likely face intensified margin headwinds. Case in point: Walmart highlighted that tariff-related costs are increasing as they restock their inventories. Finally, the Financials sector could benefit amidst Fed rate cuts if the yield curve were to steepen further from here. Bottom line: selectivity will be key.

- Bonds Investors Have Reason To ‘Cheer’ | The bond market is on track for another summer of above-average performance. The Bloomberg US Aggregate Index is up around 3%—nearly twice the typical summer return of 1.6% seen over the past 20 years. Corporate credit is also outperforming, with investment grade bonds returning 3.7% and high yield bonds up 3.5%. With yields still near their highest levels in over 15 years, income continues to be a key driver of returns—even as rates remain in a relatively contained range.

Looking ahead: With growth slowing, labor demand showing signs of strain, and less inflation from tariffs than initially feared (at least, so far), markets are increasingly expecting the Fed to restart its rate-cutting cycle after a long pause. We agree. With the fed funds rate still mildly restrictive, the Fed has sufficient room to ease to bring the fed funds rate down to a more neutral setting. The next round of employment and inflation reports will be key. Meanwhile, we still expect 100 bps of rate cuts between now and the end of next year. Notwithstanding occasional hiccups that could come from elevated supply and ongoing fiscal concerns, we believe that bonds are well- positioned to deliver solid returns in the year ahead.

View as PDF

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.